Financial Advisor

How Do I Know If My Financial Advisor Is Doing a Good Job Each Year?

We are in the spotlight

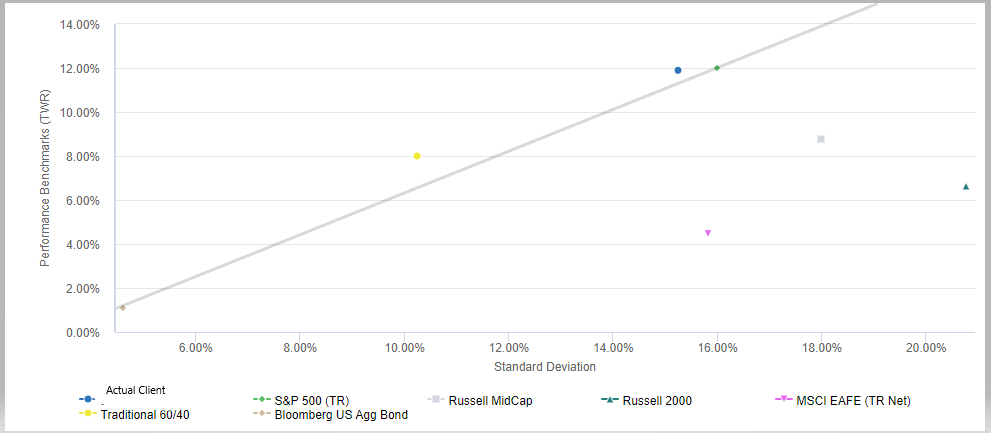

Is your financial advisor legit, or just run-of-the-mill? If you're like most people, you probably have an annual performance review at work. This is a time when your manager will sit down with you to discuss your performance over the past year. They'll talk about your strengths and weaknesses and give you feedback on how to improve. It's also a time when you gather your accomplishments, assess your progress, and reflect on your goals — a chance to determine how well you're performing and if you're on track for success. If you've hired a financial advisor, shouldn't they expect something similar? After all, you likely pay them well, and they play a crucial role in shaping your financial future. Just as you are held accountable in the workplace, it's essential to apply the same scrutiny to your advisor's performance. But how exactly can you do that? How do you know if your advisor is doing a good job each year? What are the key performance indicators (KPIs) that you can use to assess your advisor each year? Mike Absher, CIMA, CPWA, founder and managing member of Absher Wealth Management, brings the following thoughts to the discussion: “Your advisor should provide you with risk and return comparisons. There are many ways to do this, but we like to teach our clients the concepts of Alpha and Beta, and also use scatterplots on our performance reports that show returns with standard deviation for their overall portfolio versus six relative benchmarks. During our in-person reviews, we draw the capital market line and help them see whether their portfolio returns were acceptable based on the actual volatility that we exposed them to. We go through those questions because ultimately a client needs to know what they are earning, how much risk they took to earn it, how much they are paying for that process, and how likely those results are to be repeated. We find that investors who understand and believe in their portfolio strategy are much less likely to make a behavioral mistake during bear markets and also bubbles. Additionally, we believe investors should have financial planners and portfolio managers that work in unison with each other, so that portfolio decisions do not get made based on backward-looking planning software but that probability-based stress tests still affirm the approach taken to be a prudent one. We also believe that investor education is a critical element of a positive wealth management experience.” The first step toward reviewing your advisor is to get a clear understanding of what you are paying. Unfortunately, compensation can be a tricky subject when it comes to financial advice, so this could require some legwork. But, understanding how much your advisor is charging you is a critical piece of information when evaluating their services. Typically, your advisor will be paid in one of three ways. Your advisor will either get paid a fee directly by you (fee-only) or receive commissions from a third party when they sell you financial products (commission-based.) Or some advisors receive a combination of both, also known as fee-based. The easiest way to figure out how much your advisor is charging you is to ask them directly. If they are fee-only, they will likely quote your fee in terms of a percentage of your total invested assets, typically around 0.50 percent to 1 percent per year. For context, if you have $600,000 invested and pay a 1 percent fee, that's $6,000 per year in fees or $500 per month. ($600,000 x 0.01 = $6,000) Keep in mind with a percentage fee, you will end up paying more over time as your investments grow. If you started with $300,000 invested but now have $600,000 invested, your fee has doubled over time. For commission-based advisors, the fees will be a little trickier to figure out since they can range widely depending on the types of products they recommend. Again, to avoid confusion, the best advice is to directly ask your advisor, "What did I pay in fees last year?" While this can feel uncomfortable for some, it is a critical piece of information as you conduct your annual review.

Here Are 5 Ways To Know If Your Financial Advisor Is Doing a Good Job Each Year

1. Understand What You're Paying

A financial advisor does more than just manage your money. They help you get your finances in order both for today and in the future.

Use AdvisorCheck to find the best financial advisor to help you get your life on track.

One of the standard services advisors offer is investment management. But interestingly enough, there are many different strategies and investment methodologies that advisors use — some pick individual stocks, some prefer value companies, and others focus on growth or tech companies. As you look back on the year, it’s essential to evaluate how your investments performed under your advisor’s management. But that can be easier said than done because to get an accurate picture of how they did, you have to have an accurate benchmark to compare it to. For example, when most people think of the stock market, they are actually thinking of the S&P 500 or Dow Jones, two stock indexes that are commonly used in financial news. But, the S&P contains the 500 largest companies in the US, and the Dow Jones includes just 30 companies. Here’s the problem — most financial advisors would not recommend investing in either of those indexes, as they don’t have enough diversification. For starters, neither fund has any international exposure, a critical aspect of a well-rounded investment strategy. In addition, neither fund contains any bonds, which are another critical aspect of most investors’ portfolios. So, what’s a good benchmark? It ultimately depends on how you are invested, but most advisors will recommend a stock portfolio with international diversification. If that’s the case, there are many different funds you can use, but a great one to consider as a benchmark for your stock portfolio is the Vanguard Total World Stock Index Fund (VTWAX). At a high level, this fund contains almost 10,000 stocks from countries all over the world. And you can evaluate its performance over different time periods by putting the ticker into Yahoo Finance’s search tool. But make sure when you compare it to your portfolio that you are only comparing it to the stock portion, not the bond portion of your portfolio. You will want to separate the two to get an accurate comparison. So, let’s say that you compare the two and discover that your advisor underperformed a standard index fund that you could have bought on your own. Should you fire them? Not so fast — DIY investing isn’t always the best fit. For people who have yet to retire, there could be an extra emphasis on properly identifying the return needed to achieve the objectives at hand,” says Tom Shepard, CFP, APMA, the chief executive officer and founder of shepard FINANCIAL. “A 12 percent return that misses the mark isn’t necessarily better than an 8 percent return. Saving, investing and leveraging assets are all part of helping clients achieve their goals. A customized portfolio is very closely tied to earning income, managing spending and creating the liquidity needed to access low interest rates. Your advisor should know your financial situation very well and help you evolve with your money,” Tom continued. Rather than fire your advisor for underperformance, this is a great opportunity to discuss the results. Most advisors have a certain investment strategy or methodology they are following. And the fact is, not all strategies pay off every year. So, while it can be frustrating to underperform the market in a given year, it’s more important to zoom out and view the performance of the strategy over a 5 or 10-year time period. Ultimately, this is an opportunity to discuss your investments with your advisor and give them a chance to explain why they believe this is the right strategy going forward. “Some people who may have seen their portfolios go down in both 2021 and 2022 might assume that they are working with a bad financial advisor,” says Leonard Kim of AdvisorCheck. “However, if you look at the larger picture, almost every single 401k and 403b plan held by Fidelity also went down for two years in a row. Does that necessarily mean that your financial advisor did poorly and is that grounds for termination? You have to factor in as many other variables as possible, outside of just your portfolio alone,” Leonard continued. One important aspect of investing is to ensure that your investments are aligned with your desired risk level. In other words, the risk level in your portfolio should be appropriate for your age, stage, and financial goals. And because every year that passes brings you a year closer to your financial goals, your advisor should be continuously downshifting the risk in your portfolio as time goes on. Now, that doesn’t mean they’ll make changes every year, but it’s something to keep an eye on over time. So, how do you know if your investments are allocated properly? Well, that’s tough to answer because everyone’s situation and risk tolerance is unique, but here are some rules of thumb to consider. First, a 100 percent stock portfolio is as aggressive as it gets, which most advisors would not recommend unless you are very young and very aggressive. Second, a 60 percent stock and 40 percent bond portfolio is a typical retiree’s portfolio. This is what most advisors recommend for someone in or very near retirement. Now, you likely fall somewhere in the middle. 90 percent stocks and 10 percent bonds is often reserved for the youngest and most aggressive. 80 percent stocks and 20 percent bonds is very typical for someone in their 30s, 40s, and maybe 50s, and then a 70 percent stocks and 30 percent bonds portfolio is typical for someone getting closer to retirement, maybe in their 50s or 60s. Here’s the thing — asset allocation and risk tolerance vary widely by individual circumstances, but the overarching point is that your advisor should be actively looking at when to downshift your risk and be making those adjustments over time. So, if you started working with your advisor in your 40s and are now approaching retirement but have the same investment allocation you’ve always had, that could be a red flag. You should have a clear understanding of what services you are supposed to be getting from your advisor, but reflect on the past year and review what services you actually received. For example, if your advisor's website or advisory agreement lists tax planning, but the two of you have never discussed ways to save you money in taxes, there is a clear disconnect. In addition, if your advisor says to expect 4 meetings per year, but you only had 2, keep this in mind as you review their performance. The point is: if your advisor is advertising a number of different services, from investment management to tax planning and more, those are built into the price you're paying. So if you're not receiving those services but are paying for them annually, that's a problem that should be addressed. Okay, you know what you're supposed to get, you know what you actually got, but let's take it a step further: what do you actually need? Over time, your life and circumstances are going to change. Your kids will grow up, you'll change jobs, you'll move to a new city — change is universal. And, as life changes, so will your financial situation. Maybe that new job comes with stock options, or maybe you decide that you want to help your kids get through college without taking on too much student loan debt. Whatever the case, the services you needed when you first hired your advisor might not be the services you need now. So, take some time to reflect and list out the services you could actually benefit from right now. Maybe it's college planning, maybe it's equity compensation strategies, or maybe it's both. By listing out the services you need, you can get a clear understanding of whether your advisor is going to be the best fit for you going forward. Of course, most advisors will be able to help you navigate the big stuff, like planning for retirement and investing for the long term, but not all advisors will be well-versed in the nuances of college planning or incentive stock options. So, if your situation is unique, it may be time to find an advisor that offers more specialized services. Gerri A. Harrison, CFP, EA, a financial advisor at Planning with Purpose, a division of Visions Investment Services at LPL Financial has the following thoughts: “Little has to do with the actual portfolio returns, but more in the matter of what you get. I like to ask myself, have I made the individual comfortable that they are in good hands? Do they understand if they are saving enough for all of their financial needs – saving for retirement, to stay out of debt, or for major goals like a wedding, vacation home or the down payment on a home, and for more short-term goals like a vacation or a home renovation? Are we managing risk appropriately, so that the client can sleep at night while still trying to outpace inflation and taxes? Do we understand their personal situation enough to help them manage their financial behaviors in times of stress, a crisis or an unexpected event? For me, it’s all about my client – the value is not in the actual performance, it is in the relationship that is developed and making sure the client actually gets what they need.” Jon Sudkin, a private wealth advisor at Integrated Financial Partners says, “Financial advisors need to be good listeners. Clients will tell you what’s on their mind, however if all the advisor does is talk, the client won’t be able to do so.” Michael V. Sergi Jr., CFP, CRCP, a financial planner and the managing director at Ameriprise Financial Services backs this sentinment. “I believe the best advisors are the ones who sincerely care for their clients and their client's success. How to know that is more about intuition, but a good start would be an advisor that spends more time listening, and less time talking,” Michael continued. In a survey of more than 1,400 financial advisors, Financial Advisor Magazine found that the #1 reason clients fired their advisor is because their advisor failed to communicate with them. The results are clear: communication is key to a successful relationship. So, take some time to reflect on your advisor's communication over the past year. Consider the low-hanging fruit: And more than that, did they get back to you in a timely manner, or did it often take up to a week or more to hear back from your advisor? In addition, were they proactively reaching out to touch base during periods of economic uncertainty, or did they leave it up to you to initiate a discussion? Think back to some of the more stressful economic times in recent history, did your advisor reach out to reassure you, or did they wait for you to contact them? Overall, are you pleased with the level of communication you've received? If not, it may be worth considering a new financial advisor. After all, the relationship between you and your financial advisor should have clear and open communication lines. An advisor who is communicative, responsive, and knowledgeable can make a world of difference when it comes to reaching your goals, but the opposite is also true. “A financial advisor should be measured by the level of service that they provide,” says Mark Johnson at Heartland Wealth Management and Concurrent Investment Advisors. “A telltale sign that an advisor is doing a good job is that you know when you’re scheduled for a portfolio review. Your advisor should have a systematic process for reviewing your accounts on a regular basis with you and you should know what that process is. I review results with my clients at least every six months: their birth month and six months after.” Mark continued. In the end, as you wrap up your annual review, reflect on what you've found. How much are you paying your advisor, and does that align with the industry average? In addition, are you getting all the services you're supposed to get, or is there a bit of a disconnect? And more importantly, does your advisor even offer the services that you need at this point in your financial journey? From there, do you feel confident knowing that you're working with a fiduciary, or is your advisor held to a lower suitability standard? And lastly, are you happy with your advisor's communication over the last year, or did it leave something to be desired? These are all essential questions to consider when looking at the performance of your advisor. And if you're feeling unsatisfied or uncomfortable with any of the answers you come up with, it may be time to consider other options. That's where AdvisorCheck comes in. It's the most comprehensive and user-friendly resource for researching the best financial advisors in your area. And with a free membership, you can access detailed reports on each advisor and compare them side-by-side to find the one that best fits your needs. You'll be able to see how they are registered, what services they offer, their different areas of expertise, and much more. So don't wait — sign up for a free membership today to start taking advantage of all the great features AdvisorCheck has to offer. Written by Anders Skagerberg, CFP® Fact checked by Billy Quirk Reviewed by KJ Kim2. Evaluate Investment Performance

3. Reflect On Investment Risk

4. Compare What You're Supposed to Get Vs. What You Actually Got Vs. What You Actually Need

5. Reflect On Their Communication

Don't Be Afraid To Shop Around

Your go-to source for:

- Breaking out from living paycheck to paycheck

- Countering inflation with saving hacks

- Saving for your or your kid’s futures

- Turning home ownership from a dream into a reality

Disclosure The information provided in this article was written by the research and analysis team at AdvisorCheck.com to help all consumers in their financial journeys, by providing the resources and the insights to help improve one’s financial health, make it through recessionary and inflationary periods of time, and save their earnings to use them towards building a secure financial future. Unauthorized reproduction or use of this material is strictly prohibited without prior approval. Any parties interested in content syndication, references, interviews, or PR, please contact our marketing team at marketing@aimranalytics.com AdvisorCheck.com is an independent data and analytics company founded on the principles of helping to provide transparency, simplicity, and conflict-free information to all consumers. As an independent company providing conflict-free information, Advisorcheck.com does not participate, engage with, or receive funding from any affiliate marketing programs or services. To become a free AdvisorCheck member, visit advisorcheck.com/signup

Most read

The content of video and blog articles are for informational and entertainment purposes only and do not constitute investment, tax, legal, or financial advice. Always consult with a qualified professional before making any financial decisions. The views expressed are those of the author and do not reflect the opinions or recommendations of any affiliated entities.