Blog

Financial Advisor

What Does the Amount of Clients and Client Assets That Investment Firms Like Morgan Stanley, Edward Jones, Goldman Sachs, and Small to Mid-Sized Firms Have Mean?

We are in the spotlight

If you're considering hiring a financial advisor and, by extension, working with the investment firm where that advisor works, one factor to consider when making your decision is the firm’s number of clients as well as the amount of client assets they have under their management. For instance, leading investment firms like Morgan Stanley, Edward Jones and Goldman Sachs have enormous amounts of clients and client assets under management, while small to mid-size firms have quite a bit less – which may be a benefit, depending what you’re looking for in an advisor. This metric can provide insights into the firm's reputation, expertise and ability to manage your investments effectively, but we’ll explain why it’s not a be-all and end-all. We will explore what the amount of clients and client assets that an investment firm has actually indicates, as well as how you can use that info to decide which firm to work with and choose a financial advisor. Want to compare firms on your own? Get a free AdvisorCheck membership. Before we address the question of what these metrics actually mean, we’ll provide some context by showing you exactly where three of the largest and best-known investment firms stand as of March 2023. We’ll include not only their number of clients and assets under management, but also some additional metrics that help to illustrate the massive scale of these firms:A higher number of clients and assets under management generally indicates a more established and successful investment firm with more resources to work with, which could be to your benefit. However, having more clients and assets under management doesn’t mean that an investment firm will be the best fit for your needs – and we’ll explain why.

How Many Clients and Client Assets Do Large Investment Firms Have?

Finance behemoths like Bloomberg and the Wall Street Journal make you pay to learn about finance. We share our insights to expand your financial literacy for free.

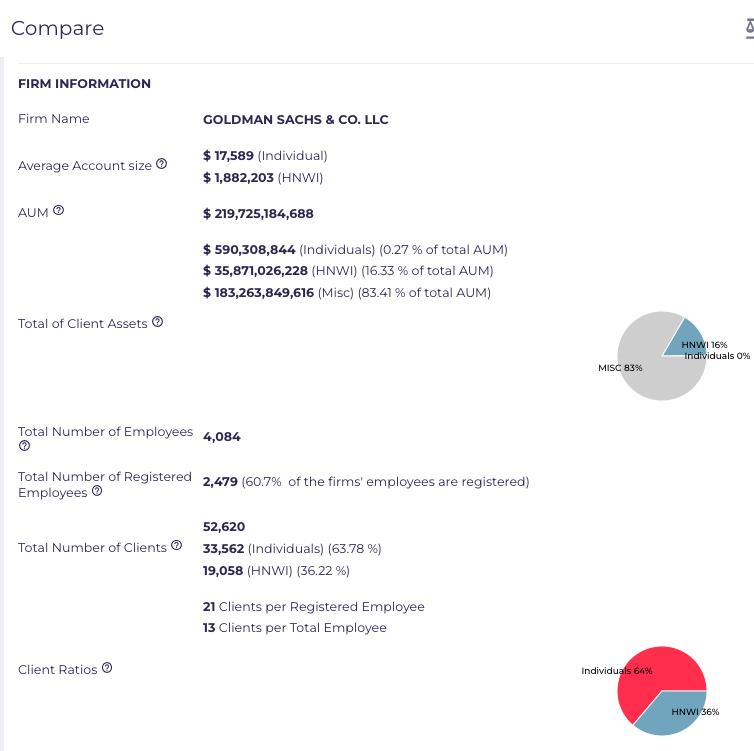

Number of clients: 2,086,037 Number of employees: 26,500 total and 15,000 registered Client ratio: 139 clients per registered employee Assets under management (AUM): $1,311,934,806,306 (more than $1.3 trillion) Average account size: $409,498 for all individuals and $12,134,751 for HNWIs (i.e., high-net-worth individuals, meaning those with at least $1 million in liquid assets) Percentage of clients that are HNWIs: 1.29 percent Number of clients: 3,242,810 Number of employees: 26,014 total and 19,444 registered Client ratio: 167 clients per registered employee Assets under management (AUM): $654,235,011,481 (more than $654 billion) Average account size: $135,651 for all individuals and $643,089 for HNWIs Percentage of clients that are HNWIs: 12.27 percent Number of clients: 52,620 Number of employees: 4,084 total and 2,479 registered Client ratio: 21 clients per registered employee Assets under management (AUM): $219,725,184,688 (more than $219 billion) Average account size: $17,589 for all individuals and $1,882,203 for HNWIs Percentage of clients that are HNWIs: 36.22 percent To make it easier for you to cross-compare the statistics for these three firms, here’s that same info in table form: These statistics demonstrate some notable differences between these three major investment firms. For instance: “When you see stark numbers like this where Goldman Sachs only has ~52,000 clients while Edward Jones has over 3 million, you can see that some firms are more selective than others when it comes to the clients they let into their network,” says Leonard Kim of AdvisorCheck. “These data points, along with what the average account size for each client, will help you be able to pick and choose which firm is best suited to help you with your financial future,” Leonard continued. Morgan Stanley

Edward Jones

Goldman Sachs

Firm # of clients # of employees Client ratios AUM Avg. account size % of HNWI clients Morgan Stanley 2,086,037 Total: 26,500 Registered: 15,000 139 clients per registered employee >$1.3 trillion All individuals: $409,498

HNWIs: $12,134,7511.29% Edward Jones 3,242,810 Total: 26,014 Registered: 19,444 167 clients per registered employee >$654 billion All individuals: $135,651HNWIs: $643,089 12.27% Goldman Sachs 52,620 Total: 4,084 Registered: 2,479 21 clients per registered employee >$219 billion All individuals: $17,589HNWIs: $1,882,203 36.22%

We empower new and seasoned investors to take charge of their finances.

Get the most reliable financial resources delivered straight to your inbox.

At this point, you may be asking yourself: do I want to work with a large investment firm that has, for instance, more than 100,000 clients and a client ratio of about 100 or more clients per advisor, or a smaller firm with a client ratio of something like 10 clients per advisor? Similarly: do I want to work with a firm whose clients are all very wealthy and have an average account size of e.g. $10 million, or a firm with more middle-class clients and an average account size closer to $50,000? We’ll explain how to make this decision and what the number of clients/client ratio really means as well as the significance of firms’ average account sizes. For starters, you’ll need to find a firm that is willing to work with you based on your net worth. Some firms might have minimum asset thresholds of $50,000, $100,000 or even $500,000 to $1 million. On the other hand, other firms won’t mind if you start an account with just a few hundred dollars. If there’s an investment firm you’re interested in working with that has minimum asset thresholds, you may need to save up to get to that point before you start working with them. Be sure not to interpret the existence of minimum asset thresholds as an indication that those with limited assets wouldn’t benefit from working with a financial advisor. It just means that some firms and financial advisors aren’t willing to work with clients who have smaller pools of investable assets, but every firm has different requirements, and those across the financial spectrum can benefit from professional guidance and advice. Just take it from Robert R. Johnson, professor of finance at the Heider College of Business at Creighton University: “I would contend that a financial professional provides a 25-year-old with limited assets more value than a 65-year-old with ample assets . . . When we get sick, we go to the doctor. When we get into legal trouble, we hire a lawyer. Yet somehow people believe that they should be able to navigate the ever increasingly perilous financial waters without professional help. Financial mistakes, particularly early in life, can be difficult to overcome and many people wait too long to establish a relationship with a qualified financial advisor. Making a few good financial decisions early in life can make the difference between a secure retirement and one fraught with difficulties.” Rather than using total assets as a metric for whether or not to hire an advisor, Scott Schleicher, financial planning specialist group manager and senior financial advisor at Personal Capital argues that the most important factors to consider in this decision are:Should You Work with a Small Firm or a Big Firm?

The First Hurdle: Minimum Asset Thresholds

The Existence of Minimum Asset Thresholds ≠ Those With Limited Assets Shouldn’t Hire a Financial Advisor

We all need help getting our finances in order throughout our lifetime.

Look through our database to find the most trustworthy financial advisors in your area.

Here are some of the key differences between smaller and larger firms: At this point, once you’ve assessed factors like their AUM, average account size, number of clients and client ratios (among others), perhaps you’ve decided to work with a particular investment firm. The next step is going to be to select and hire a financial advisor who works at that firm. AdvisorCheck is the most effective tool for locating financial advisors in your area based on their associated firm, as well as on their credentials, their disclosures and other potential criteria. Drawing on an array of top-quality sources, AdvisorCheck allows you to tap into a vast database of more than a million financial advisors. Once you’ve made a free account and used the site to find potential advisors in your area who work at the firm you’ve chosen, you can save them to your profile (you can find your saved listings here) and use the site’s Compare tool to weigh their histories against each other. How do you do this? Start by heading to AdvisorCheck’s advisor search page and entering your location and the firm you’ve chosen. While you’re scrolling through the results, add up to three advisor profiles to the Compare tool at a time by clicking the scales symbol at the bottom of each advisor’s listing. Then, navigate to the Compare page by clicking the link on the left-hand sidebar. You’ll see a detailed comparison of the advisors you’re considering, including: All of this info is enormously helpful when you’re deciding which advisor fits the criteria for what to seek out in a financial advisor, as well as what to avoid. By providing the most essential details laid out in an easy-to-read comparison, the AdvisorCheck Compare tool could slash an estimated 80 percent (or even more!) off the time you spend researching. And once you’ve hired an advisor, AdvisorCheck even makes it easy to keep track of any changes to their profile. Saving your advisor to your AdvisorCheck profile means you can see when something like a disclosure is added to their history, so you can monitor the person you’ve entrusted with managing your money on an ongoing basis and enjoy greater financial peace of mind. Empowering yourself with information is the most effective way to ensure that the financial advisor you choose is skilled and trustworthy – someone who consistently prioritizes their clients’ best interests. AdvisorCheck makes it possible to choose an advisor who can effectively manage your finances, maximize your investment potential, establish practical short- and long-term plans and serve as a springboard to achieving your financial goals. Sign-up for your free AdvisorCheck membership and start comparing financial advisors and their firms now. Written by Billy Quirk Fact checked by Luke Jara Reviewed by KJ KimComparison: Smaller Firms vs. Larger Firms

Smaller Firms Larger Firms Don’t always have the resources to meet all their clients’ needs in-house More resources at their disposal and a wider range of in-house experts (e.g., specialized attorneys), so they don’t have to refer clients to external specialists as often Tend to have less of a back-up system if your advisor is absent (e.g., while they’re on vacation) or stops working there Typically have more robust back-up systems and succession plans if your advisor is absent or stops working there Limited access to certain kinds of investment opportunities More access to some kinds of valuable investment opportunities, such as initial public offerings Allow clients to “get the personalized service and advice they deserve,” according to certified financial planner Howard Pressman Large size can make their clients feel like a number, with less personalized service and more cookie-cutter advice Have more time for their smaller clients Tend to focus more on big clients (HNWIs) and pay less attention to their smaller clients May have lower minimum asset thresholds, or none at all Often have higher minimum asset thresholds They “might have more flexibility to deal with the idiosyncrasies of your portfolio,” according to Christine Benz, director of personal finance for Morningstar Have less flexibility in the investment opportunities that they can offer Benefit your local economy by supporting a small business Offer fewer benefits to local economy More likely to be “well versed in community issues regarding taxes and incentive programs” (source) Less familiarity with community-specific taxes and incentive programs Less likely to offer investment products that create a conflict of interest May offer investment opportunities/products that create a conflict of interest if they offer commissions for the broker Clients are less likely to be offered products they don’t need to satisfy shareholders Clients may be offered products due to “the need to earn a quarterly profit to satisfy shareholders,” which “can translate into pressure to sell products, regardless of whether clients need those products,” writes Forbes The Wealth Management Luxury Brand Status Index survey found that smaller firms have “reputations for honesty and superior client service” Less reputation for honesty among consumers Often have lower overhead costs, which means clients pay lower fees Higher fees due to higher overhead costs on average More nimble, meaning they can react more quickly to changes in the market, taking advantage of investment opportunities and avoiding potential pitfalls Less nimble and thus less able to react quickly to market changes Use AdvisorCheck to Find Skilled Financial Advisors at Your Investment Firm of Choice – and Then Compare Them

Your go-to source for:

- Breaking out from living paycheck to paycheck

- Countering inflation with saving hacks

- Saving for your or your kid’s futures

- Turning home ownership from a dream into a reality

Disclosure The information provided in this article was written by the research and analysis team at AdvisorCheck.com to help all consumers in their financial journeys, by providing the resources and the insights to help improve one’s financial health, make it through recessionary and inflationary periods of time, and save their earnings to use them towards building a secure financial future. Unauthorized reproduction or use of this material is strictly prohibited without prior approval. Any parties interested in content syndication, references, interviews, or PR, please contact our marketing team at marketing@aimranalytics.com AdvisorCheck.com is an independent data and analytics company founded on the principles of helping to provide transparency, simplicity, and conflict-free information to all consumers. As an independent company providing conflict-free information, Advisorcheck.com does not participate, engage with, or receive funding from any affiliate marketing programs or services. To become a free AdvisorCheck member, visit advisorcheck.com/signup

Most read

The content of video and blog articles are for informational and entertainment purposes only and do not constitute investment, tax, legal, or financial advice. Always consult with a qualified professional before making any financial decisions. The views expressed are those of the author and do not reflect the opinions or recommendations of any affiliated entities.